Financial support to workers affected by the Covid-19 crisis

The TWSS ceases on the 31st of August and is replaced by the Employment Wage Subsidy Scheme (EWSS).

The Temporary Covid-19 Wage Subsidy Scheme (TWSS) provides financial support to workers affected by the Covid-19 crisis.

It’s designed to help employers and businesses that are significantly impacted by the Covid-19 pandemic (check out our Covid updates for businesses). It provides employers with financial support to pay their employees through their payroll system during this crisis.

What should employers do?

If you qualify for the Temporary Covid-19 Wage Subsidy Scheme, the first thing you should do is send a MyEnquiry to Revenue through ROS.

If you outsource your payroll, you should contact your service provider and let them know your situation so they can amend your payroll and submit the MyEnquiry on your behalf.

Talk to our Client Services Team if you want more information about how we can help businesses in Ireland overcome the Covid-19 challenges.

Who is eligible for this scheme?

Business critera

- All employers across all sectors excluding the Public Service and Non-Commercial Semi-State Sector.

- Businesses experiencing a significant negative economic disruption due to Covid-19.

- Businesses that have lost or are likely to lose at least 25% of turnover.

- Employers who are unable to pay normal wages in full.

Employee criteria

- Employees need to be on the employers’ payroll from 29 February 2020 and a payroll submission needs to have been made from 1 February 2020 to 15 March 2020.

- Workers returning to work after a period of Maternity, Paternity, Parental, Adoptive or related unpaid leave.

- Employees who were laid off after 29 February 2020 may be taken back onto the payroll system for the purposes of this scheme.

- There are no age restrictions for employees under this scheme.

- Fulltime, part-time and short-time workers are eligible to be paid under this scheme.

- Company Directors are included in this scheme if they are paid a salary.

Who is not eligible for this scheme?

- Sole Traders / self-employed people are paid directly by DEASP under Covid-19 Pandemic Unemployment Payment.

- Employees also receiving payment from the DEASP, (e.g. Pandemic Unemployment Payment), cannot also receive payment under this scheme.

- Employees not on the payroll system from 29 February 2020 and/or not received a payroll submission during the period of 1 February 2020 to 15 March 2020 cannot avail of this scheme.

What about workers returning to work after a period of maternity or adoptive leave?

On the 29th May 2020, it was announced that ” a change to the Temporary Wage Subsidy Scheme (TWSS) will be made to accommodate the salaries of those who have returned to work after a period of maternity or adoptive leave and who may not have been on the payroll of their employer on 29 February, or been paid in either January or February 2020.”

Revenue has agreed that this provision will be implemented from 26 March, where applicable.

How can I prove significant negative economic disruption?

In most cases, significant negative economic disruption will be obvious.

For example, some businesses have had to close their premises, there have been restrictions on trade, physical distancing has been implemented nationwide and the impact of essential and non-essential businesses has resulted in the significant negative economic disruption.

There is no one way to prove to Revenue that there has been significant negative economic disruption. So we recommend you keep all evidence, such as website traffic records, cash flow forecasts, sales and revenue figures, client contracts, and anything else that you or your accountant deem appropriate to prove your business’ significant decrease.

Examples of significant economic disruption

Although Revenue is not looking for proof of qualification for the scheme yet, employers availing of this scheme should still retain all evidence that explains why they are entering this scheme:

- Documentation that turnover is likely to decrease by 25% for April, May, June 2020

- Statements to indicate that the business is unable to meet normal wages or normal expenses

- Records that show a decline in orders in March 2020, in comparison to February 2020

- Documentation submitted to a financial institution as part of the negotiation of loans or overdrafts

- Notifications or communications to staff regarding salary/wage cuts implemented as a direct result of Covid-19

- Evidence of reliance on the Government Credit Guarantee Scheme or overdraft facilities or other borrowings for capital purposes

- In the case of Startup businesses, an example would be evidence of a decline in investment by at least 25% arising from the crisis

- Any other examples that have relevant evidence to support the declaration

How to calculate how much to pay employees under this new scheme?

Under this new scheme, Revenue will refund employers up to a maximum of €410 per week per qualifying employee.

The amount of refund will depend on how much you normally paid each employee before this pandemic.

The subsidy amount is calculated at a rate of 70% of the employee’s average net pay (i.e. after taxes) in January 2020 and February 2020.

Employers can make “top-up payments” on top of the subsidy payment to help maintain as close to 100% of normal income as possible for the subsidised period.

This is an optional payment and if employers do not wish to make any additional payments, they can put €0.01 as the Gross Pay amount.

What changes do I need to make to the payroll process?

Employers run payroll as normal but the following details should be entered for any qualifying employee under the scheme:

- PRSI class should be set to J9

- A non-taxable amount equal to the employee’s net take-home pay or €410, whichever is lesser (i.e. you do not deduct income tax, USC or LPT, if applicable, or PRSI from the subsidy amount).

- If the employer is not making any payment to the employee, they should include a payment amount of €0.01 in the Gross Pay.

- If an employer is making additional wage payments, they should include this amount in Gross Pay.

- Employers do not include the Temporary Wage Subsidy payment in gross pay (i.e. €410).

- The payroll submission must include pay frequency and period number.

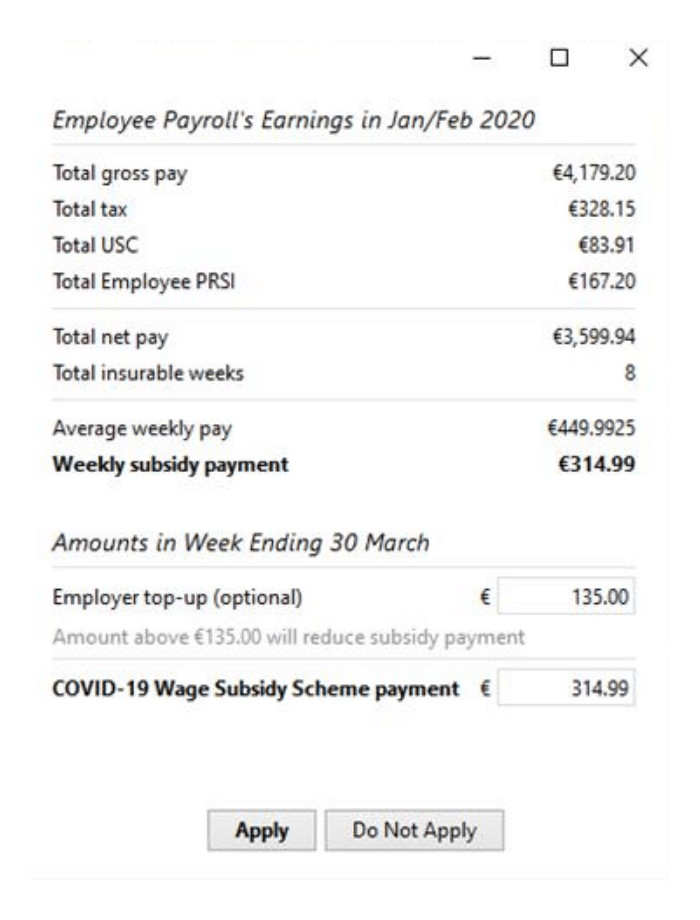

Example payroll submission

We use payroll software called BrightPay Connect to process payroll for our clients. Many software, such as Connect, will update their systems to reflect these new changes automatically.

If you process your payroll on ROS, Revenue has also made adjustments for this new scheme.

If you need help with processing payroll, talk to our Client Services Team about outsourcing your payroll.

You can also join our free, live Covid-19 Q&A webinar for businesses in Ireland.

The below example is based on an individual on minimum wage working 40 hours a week using the BrightPay Connect software.

- Total gross pay = total gross pay in Jan 2020 and Feb 2020

- Total tax = total tax paid in Jan 2020 and Feb 2020

- Total USC = total USC paid in Jan 2020 and Feb 2020

- Total Employee PRSI = total Employee PRSI paid in Jan 2020 and Feb 2020

- Total net pay = total amount to be paid minus taxes

- Total insurable weeks = number of weeks in Jan 2020 and Feb 2020

- Average weekly pay = total net pay / total insurable weeks

- Weekly subsidy payment = 70% of average weekly pay

- Employer top-up = the amount the employer will contribute to helping maintain as close to 100% normal income for the employee

- Covid-19 Wage Subsidy Scheme payment = amount to be refunded by Revenue

Are there any limitations to this scheme?

- The employer’s name and address will be published on the Revenue website. Revenue states that “This is a fairly standard approach to any type of grant process. Effectively the register will be available on the Revenue website after the scheme has finished.”

- There is a Euro for Euro reduction in the wage subsidy amount for any excess paid on top-up amounts.

- The maximum subsidy payment is €410 per week, which the equivalent of an average net weekly pay of less than or equal to €586.

- There is a maximum of €350 per week where the average net weekly pay is greater than €586 and less than or equal to €960. In other words, if workers earn more than an average of €960 net pay per week, the wages are not entitled to be subsidised under this scheme.

What does this mean for the employer?

The bottom line here is that employers should not end up paying staff more than their normal weekly or monthly net pay under this scheme.

Although employers are asked to use their best efforts to maintain an employee’s normal wages during this time, it’s important that the employee does not exceed their normal rate of pay.

Revenue is very clear in that they say that employers will face penalties if there is any abuse of this scheme, such as self-declaring incorrectly, not providing funds to employees, or non-adherence to guidelines.

If you have any questions about your payroll process, please contact our Client Services Team for a quotation for our Payroll Services.

You can also join our Covid-9 Q&A webinar with our Chartered Accountants and a special host from HR Team.

What taxes need to be paid?

Revenue will not apply income tax or USC on the subsidy during this period, however, this will be reviewed at the end of the year and income tax and USC on the subsidy may become liable at that point.

Income tax and USC

Income tax and USC will not be applied to the wage subsidy payment in real-time. However, it will apply to any top-up payments.

Employee PRSI

Employee PRSI will not apply to the subsidy or any top-up payment by the employer.

Employer’s PRSI

Employer’s PRSI will not apply to the subsidy payment and will be reduced from 11.05% to 0.5% on the top-up payment.

Revenue Compliance Programme

From mid-June 2020, Revenue will carry out compliance checks on all employers availing of the TWSS. Each employer will receive a letter, generally through MyEnquiries, to confirm the following:

- Businesses meet the eligibility criteria – this includes an outline of the nature of your business, its principal activities, a summary of the impact of the Covid-19 restrictions on the turnover of your business.

- Employees are receiving the correct subsidy amount – this includes details of who runs your payroll, confirmation that all payslips were issued correctly

- The subsidy amount is being recorded correctly – this includes copies of gross net reconciliation and confirmation of EFT for net pay from your bank account

Revenue states “it is essential that employers respond promptly as failure to do so may lead to suspension of future payments.”

What if an employee was not on payroll in January or February 2020?

If there is an individual who was employed by the business in January or February 2020 but did not receive normal pay during this period, the employee can decide not to participate under the Temporary Covid-19 Wage Subsidy Scheme.

These employees can choose to apply directly to DEASP for the Covid-19 Pandemic Unemployment Payment.

Employers and employees should discuss this option and come to an arrangement on how to proceed in this case.

Alternatively, you can speak to your accountant or Payroll Specialist on the different options available.

What if employees were paid different amounts in January and February 2020?

The subsidy amount is based on the weekly average net pay. This means that the calculation is based on the average of payments made in January and Februay 2020.

Does this scheme apply for the whole month of March?

This scheme applies from 26th March, for payroll submissions on or after 26th March. The exception to this is any payroll for the week commencing Monday 23rd March.

Any submissions before the 26th March will not be processed under this scheme but they are covered by the previous Employer Covid-19 Refund Scheme. This old scheme entitled employers to a refund of €203 per week per qualifying employee.

Does this scheme apply for payroll in April?

Yes. The scheme started on the 26th of March and will run for an initial period of 12 weeks.

This may even be extended further. We will update this with more information when it is available.

I use payroll software, will it implement these changes automatically?

We are now in the operational phase of this scheme which involves subsidy tapering.

This may not be applied automatically by all payroll software packages. Once you download the Employer CSV file from ROS you can:

- Import this information into payroll software and the payroll software will use this

information - Use the information outside of payroll software along with the new rates and any Additional Gross

Payment (top-up) amount, to calculate the wage subsidy for each eligible employee.

Talk to us about outsourcing your payroll if you would like us to take care of this for you.

Can I rehire an employee to avail of this scheme?

We have moved into the 2nd phase of the TWSS and therefore any employee that is rehired after 1st May 2020 will not be included in the scheme.

J9 submissions for employees rehired after 1st May will be rejected. However, Revenue expects they will reprocess all the submissions received from the employee’s rehire date and refund where appropriate at a future date.

I'm an employee, not an employer, what do I need to do?

Employees do not need to do anything under TWSS as it is the employers’ responsibility to apply through ROS.

However, employees may decide not to participate in this subsidy scheme and avail of the Covid-19 Pandemic Unemployment Payment directly from the Department of Employment Affairs and Social Protection (DEASP).

Read more about this pandemic payment on our blogpost – Important Updates For Businesses Impacted By Covid-19

What about cross-border workers?

The Temporary Wage Subsidy Scheme will generally apply to cross-border workers as long as there is an Irish contract of employment.

If you have more questions about this, please speak to your accountant or payroll provider. If you would like to outsource your payroll, please contact our Client Services Team.

Who receives the refund and where is it paid?

Under this scheme, employers will still pay employees through the normal payroll process.

Employers will receive a refund from Revenue normally within two working days.

The refund will be deposited directly into the employer’s bank account.

Are workers entitled to this scheme if they have multiple jobs?

Under the transitional phase (phase 1), if an employee has multiple jobs, each employer could operate the scheme based on 70% of their net weekly earnings.

We have now moved to the operational phase (phase 2 – from 4th May 2020). Earnings from all active employments will now be combines and reconciled. Each employer will have personalised information on their employee’s wage subsidy amount and it will take the employee’s overall position into account when calculating their subsidy entitlements.

Should I make payroll submissions early to ensure I get the refund as soon as possible?

The normal payroll process is that the payroll submissions must be made to Revenue on or before the day the employee is paid.

Under these guidelines and the introduction of the new subsidy scheme, Revenue states that if a payroll submission is made more than 4 days in advance of the pay-date, Revenue will not process the refund until 4 days before the pay-date.

This is to make sure that employees Revenue Payroll Notification (RPN) is entirely accurate before the refund is paid.

What if bonuses, commissions or other payments were made to the employee in Jan and Feb payroll?

Bonuses, commissions and other payments will be taken into account in the calculation if these were included as part of gross pay in the January and February 2020 payroll submissions.

Can I deduct pension contributions from the wage subsidy?

No, the pension contribution cannot be deducted from the wage subsidy amount. The employer must pay the subsidy amount to the employee in full.

What should I do if I receive too much money from Revenue?

As mentioned, during the first phase, Revenue is refunding €410 for each qualifying employee regardless of their average net weekly pay. This means that there will be some excess paid into employers’ bank accounts.

Employers should keep the following:

- Records of subsidy payments to employees

- Records of subsidy refunds and tax refunds received from Revenue

- Hold any excess of the subsidy payments received to be offset against future susidy payments or future repayment to Revenue

Need help?

If you need help with your payroll system, talk to our Client Services Team now.

We’re happy to talk to you about outsourcing your payroll. Call us on +353 (0)1 905 9364 or email hello@accountantonline.ie.

Kiera leads the Bookkeeping, VAT, and Payroll Teams at Accountant Online. Kiera has worked in the financial services industry for over 18 years. She is passionate about helping businesses to get their finances in order so they can get back to what’s important: running your business. Kiera holds a part-qualified accountant qualification from ACCA.